Several Founders, Co-Founders, CXO Bankers, CXO Fintech professional & people who participated in the ePanel discussions:

- Mr. Nilay Arora, Country Head & VP- Tencent

- Mr. Vinod Shah, CIO, and GM, Gujarat State Co-operative Bank Ltd

- Mr. Sheoji Meena, General Manager, Bank of India

- Mr. Probir Roy, Co-founder, Paymate

- Mr. Taron Mohan, CEO & Promoter, NextGen Telesolutions Pvt Ltd

- Mr. Shashank Chowdhury, Former Executive VP- Inclusion Initiatives, Vakrangee Software Ltd

- Mr. P B Prakash, Head-Financial Institutions Group, IndusInd Bank

- Mr. Monica Jasuja, Former Head of Digital & Emerging Partnerships, Mastercard

- Mr. Anil Shenoy, Director and Risk Management, First Data Corporation

- Mr. Ajay B Panicker, CEO & Founder, NetPay Limited

- Mr. Raghu Veer Dendukuri, Founder, Ideal Nation, and Solution Architect at Invincible Tech Systems Inc.

- Mr. Aishwarya Jaishankar, SVP – Digital Products & Platforms, HSBC

- Mr. Ruchit Jangid, Former Business Head, SOTC Travel Ltd

- Mr. Rakesh Shetty, Product Head Micro Loans, Fortune Credit Capital Ltd

- Mr. Subbiaa Olimuthu, former Product Manager – RuPay Product

- Mr. Kamonasish Aayush Mazumdar, Founder & CEO at Foodieverse

- Mr. Vikas R Panditrao, Co-Founder, Forum of Industry and Academic Knowledge Sharing (FIAKS)

- Many other CEO/CXO Bankers & Fintech professionals on FIAKS Forum requested to remain anonymous

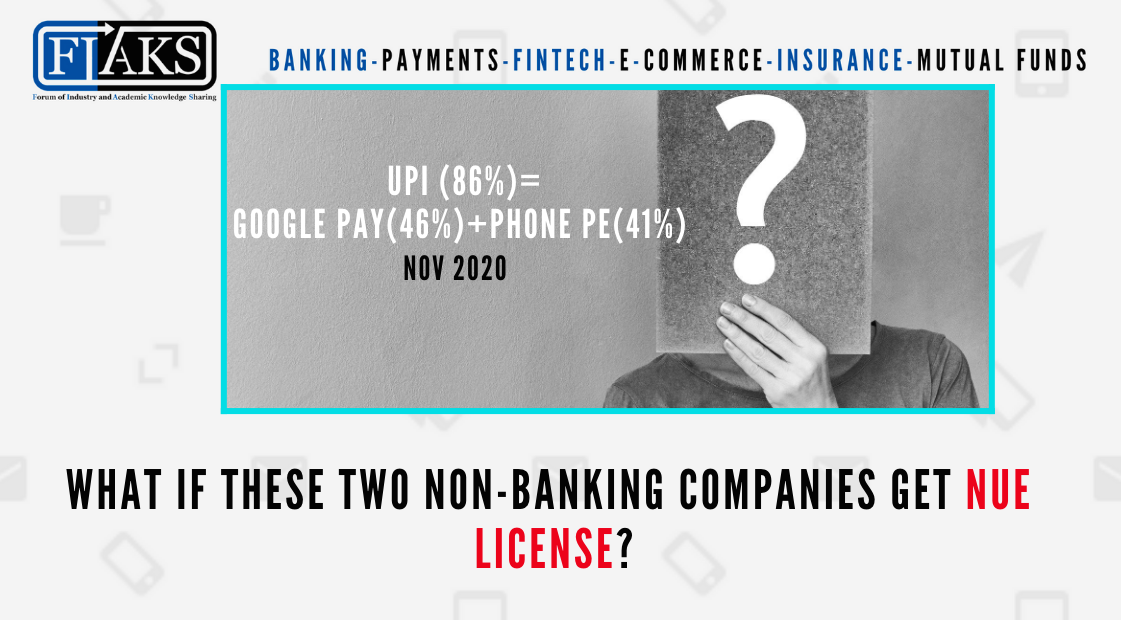

Here’s something to take note of; NPCI (UPI) 86% = Google Pay 45% + PhonePe 41% (for Nov 2020). [1] Isn’t something injudicious? Is RBI taking a note of possible risk as both are non-banking entities? Here are some pondering questions;

Question 1: What happens to NPCI if these two companies launch an NUE entity of their own? NPCI transaction count will be only 14%.

- A member opines, “I think it is UPI which driving them and not the other way round. So even if they quit and create their own, depending upon their joint product, you may see their future growth, however, UPI is here to stay and will only grow.”

- For an NUE to start, create a UPI-like product and take off is a big ask, another 2-3 years away even in the best case. Failure at NPCI is a common bane right, won’t be different for any player.

- To launch an NUE for these two companies it would certainly take some time. In the meanwhile, NPCI and the member banks would also work on smoothening the rough edges and come out clear and effective competitors. So, saying if they leave NPCI would be left with 14% is a rather simplistic analysis.

- On the contrary, a member opines, “UPI numbers are being driven by the private VC funded companies and not any bank or NPCI. This is confirmed by the transaction volumes. So the success of UPI ought to be 100% attributed to the private companies and not NPCI – NPCI is only an enabler of the ecosystem. Why aren’t these fintech players being given their due share of acknowledgment in any post/article?”

Question 2: If funding to these two companies stops what happens to transaction count? Are these two companies (Google Pay & PhonePe) profitable?

- Nothing happens when an entity ceases to exist in UPI, as long as at least one entity exists

- No payments company working in pure UPI is making money, their objective is to make money on payments data. So funding won’t stop as payment data will be leveraged for revenues to value add these companies will provide to their merchants.

- If funding stops for these two companies stop, the UPI payment space would not be left orphaned. There would be players to take it up from where they leave. Business Continuity Plans would kick in.

- Payment is an eternal business that will never turn redundant. Only the mode of payment will undergo changes. So one or two companies going out of business will not matter though it is doubtful if either GPay or Phonepe will get that fate. Payment is the ultimate data source as one learns a great deal about users, finances, lifestyle, and choices. Even if they do, there will be others to take their place.

Question 3: Bank product offerings are equally good, why are they not getting transactions? Banks have restrictions on payouts for promotion up to Rs 250/-. What about these two companies? Are regulators checking their marketing spends?

Register and read the complete bespoke discussions