Several Founders, Co-Founders, CXO Bankers, CXO Fintech professional & people who participated in the ePanel discussions:

- Mr. Prasanna Divekar, Principal, Renaissance India Partners

- Mr. Suresh Gurumani, MD & CEO, PetroMoney Fintech

- Mr. P B Prakash, Head-Financial Institutions Group, IndusInd Bank

- Ms. Tanya Naik, former Director, Payments, PayPal Payments Private Limited

- Mr. Abhishek Arun, Chief Operating Officer, Paytm Payments Bank

- Ms. Aishwarya Jaishankar, Co-Founder, Hyerface Technologies

- Mr. Alok Karkera, Former Head – India Public Sector & North India Financial Institutions Group at Citi

- Mr. Anand Kulkarni, President & Program Head, Yes Bank

- Mr. Arun Tanksali, Co-founder & CTO, Nearex

- Mr. Prasad Likhite, former Director Sales, ACI Worldwide

- Mr. Ramasubramanian S, Deputy Vice President, Axis Bank

- Mr. Sugata Ghosh, Associate Editor at The Economic Times, BCCL

- Mr. Neeraj Chandra, Head of Operations and Technology, India, Abu Dhabi Commercial Bank

- Mr. Balaji Vishwanath, Head-Global Digital Acquisition, Standard Chartered Global Business Services

- Mr. Arvind Narayanan, Co-Founder, Enlearning skill development Pvt ltd

- Mr. Manish Jeloka, President & Chief Strategist, Probus Insurance Broker Private Limited

- Vikas R Panditrao, Co-Founder, Forum of Industry and Academic Knowledge Sharing (FIAKS)

- Many other CEO/CXO Bankers & Fintech professionals on FIAKS Forum requested to remain anonymous

This pandemic has already created a lot of economic chaos. Lots of businesses have shut down. Here comes another breaking news, “Citi bank exiting India and 12 more countries.” [1]

This news triggered discussions on Well, banking is regulated and exit can be managed but what happens if large fintech which is the customer-facing brand (and has no regulatory obligation) decides to exit overnight a country? Are we prepared?

Another question was ..Do you see MNC banks having any USP to compete with private or small finance banks or payments banks? Apart from just offering fat salaries to its employees?

- Member states, “If MNC banks had no value then both consumers and corporates should have walked out any time. I am sure people do know that for example, Citi’s card franchise even after so many years is still amongst the best, Citigold wealth – honestly private banking of private sector banking does not match Citi gold wealth management. The higher salaries piece – if Citi was listed in India and had ESOPs salaries could have been much lower and their valuation really good vis-a-vis their global US parent. Some of the stuff which Citi offers on corporate banking is still not available and frankly despite their consumer net banking not getting changed or upgraded for the last 15 years – it still is better and works vs some of the private sector banks in India.”

- One should look at the profit per employee numbers as reported by the banks. A Citi India for example is miles ahead of the domestic banks. That itself indicates the value that the MNC banks bring. That number also demolishes that fat salary argument.

- The profit per employee is actually lopsided towards the Corp bank doing big deals. Doesn’t seem that retail will stand the same test. Well, with so few branches, it will. It is higher than other banks, again thanks to a strong Citigold portfolio, but certainly way lower than their own Corp bank.

- Key-value MNCs have are segments like NRI and ultra-high net worth, which sadly is not tapped very well by them. Member mentions, when I was with a top MNC, noticed that so many premium customers had the account just for their global transfer feature, which allowed them to seamlessly send money for their kids’ education, etc

- A combination of regulatory constraints and the cost structure of foreign banks have limited their ability to scale up hence retail will be dominated by local players.

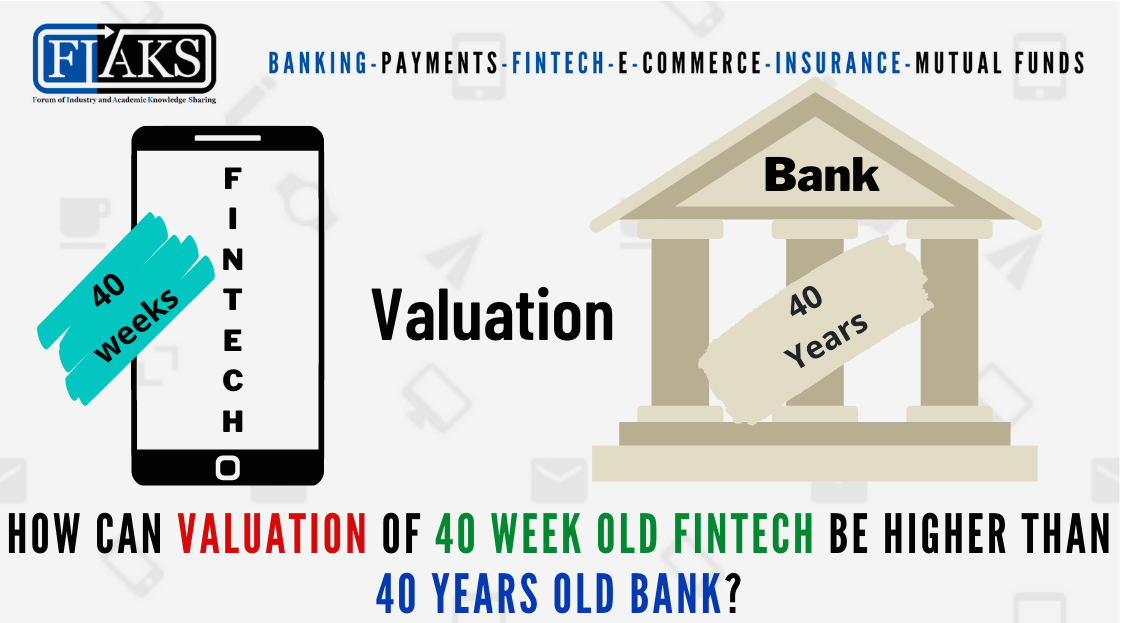

Now check this tweet out;

- Clearly the difference between 40 years and 40 weeks. A valuation can be blind. No words to say. Maybe 40 years old is the reason. Nowadays riding on someone else’s business is profitable than running your own business. E.g. Google pay, Airbnb, Cred, etc

- A member thinks this is not an accurate comparison. Citi’s retail valuation is driven by how much AUM stays with them. Most customers who enjoyed the Citi global platform benefit might not be keen to stay with a smaller bank. Attrition possibility is high. Plus, things like ATMs, Branches, etc are losing value. These businesses do not have a moat. When RBS exited certain businesses, even they got low valuation multiples. Same with Deutsche. What Cred & many other fintech are attempting to do is embed themselves in customer behavior. This is a valuable moat to build. Whether Cred builds it or not is open to debate, but they are attempting something ambitious which big money is willing to back.

- Having said that, isn’t this the price of not disrupting the market at the right time. Capital light businesses versus capital intensive businesses. How much incrementality will the portfolio bring to a potential buyer? Eg: for a buyer bank that has the distribution and reach and has invested in the latest tech, maybe the price of acquiring a great customer base is only worth USD 2 bn

- A member puts forth a contrarian/controversial thought. Enterprises are broadly of 2 types – charitable/not-for-profit and for-profit. Any investment with an expectation of monetary returns has to be linked with the profit/profit potential of the enterprise. What we are seeing with “don’t look at profits” is nothing short of a Ponzi scheme. Guaranteeing/building expectation of high returns without underlying enterprise making money by driving higher valuations is similar to “Find more people willing to invest higher than the last time so you can be paid out of those proceeds”. Unfortunately, as seen in many including WeWork is that when the buck stops, or the bell rings, we suddenly find that there is no chair to sit on (Musical Chairs). Agreeing with this point of view another member adds that said some models take time to build like Amazon, Airbnb, etc. But there are a lot of models which are questionable and only time will tell when the house of cards for some of those companies like WeWork will fall.

Now talking about unicorns;

Register and Read the complete bespoke discussions