Several Founders, Co-Founders, CXO Bankers, CXO Fintech professional & people who participated in the ePanel discussions:

- Mr. Sandeep Todi, Co-Founder & CMO, Remitr

- Mr. Devatanu Banerjee, Founder Tensor Flow User Group, Toront

- Mr Arun Tanksali, Co-founder & CTO, Neare

- Mr Rajiv Rai, former Chief Digital Officer at Edelweis

- Mr Vikram Sareen, Blue Bricks Pty Ltd, Chief Architect,Founder,CEO

- Mr. Kunal Shah, Founder, and CEO, CRED

- Mr. Naveen Surya, Chairman Emeritus, Payment Council of India

- Mr. K Aayush Mazumdar, CMO, MeraEvent

- Mr. Ajay B Panicker, CEO & Founder, Netpay Limited

- Mr. Sony A, Head – Digital, South Indian Ban

- Mr Alok Jha, Managing Director Cyberplat India

- Mr. Abhishek Mody, Associate Director-Payment & Digital Initiatives, IDFC Bank

- Mr. Avro Mukerji, Investment Counselor- NRI Burgundy, Axis Bank

- Mr. Vikas R Panditrao, Advisor, Forum of Industry Academic Knowledge Sharing (FIAKS)

- Many other CEO/CXO Bankers & Fintech professionals on FIAKS Forum requested to remain anonymous

While cryptocurrency was hailed by many to be a revolutionary concept in the world of digital currency, the sudden death of Gerald Cotton, the CEO of Quadriga, Canada’s largest cryptocurrency exchange raised several questions with regard to the risks inherent. Reports say that no one has so far been able to unlock $137 million in wallets since only Cotton knew the password, leaving clients in a quandary.

However, according to EY reports the wallets were emptied much before, in April and Dec 2018. Against the backdrop of all these several questions arise – does cryptocurrency have a future here?

As of now cryptocurrency as a form of payment is largely for the tech-savvy. Firstly, in order to understand how it functions one needs to know the digital medium well and India has a long way to go on that front. Secondly, crypto is said to be high on privacy – it could get difficult for the government to know what exactly you are buying. Besides, the risk of tax evasion also exists, scalability is yet another concern.

Cryptocurrency or virtual currency has no physical form, is transferred digitally between peers and in the absence of regulations is fraught with risks of money laundering, terrorism funding, etc. There have been several reports of MLM schemes, phishing, hacking, etc – the crimes are only increasing. India has roundabout five million traders of cryptocurrency, about 15 cryptocurrency exchanges – and the numbers are going up already.

The Indian government did consider launching a Central Bank Digital Currency for domestic payments on blockchain technology in the past but soon decided to shelve the idea since it felt it was too premature. Presently, it is contemplating a total ban on cryptocurrency, calling it a ‘Ponzi’ scheme.

However, several countries including the USA, Spain, Sweden, Japan have adopted it already. What’s more – JP Morgan Bank already has its own cryptocurrency and crypto enthusiasts are confident that cryptocurrency will soon be yet another asset class akin to real estate or gold. But will it be a reality here?

‘2018 saw a stagnation in the price of Bitcoins and the wider cryptocurrency market, but it’s safe to assume that it’s not all over yet. In a first of its kind initiative, in Feb 2019 JP Morgan announced the trial launch of “JPM Coin” the first real-world use of a digital coin by a major U. S bank’ (Source: CNBC.com)

FIAKS, a knowledge-sharing community of experts from banking, fintech, payments and e-commerce in India opines about the future of cryptocurrencies in India.

Says an industry expert, “Closer home the RBI has not shown any love for cryptocurrency and has placed a ban on it. We have to wait till July’19 for the Supreme Court ruling on cryptocurrencies. If we are to take the latest development where RBI has excluded cryptocurrencies from its regulatory sandbox framework, then the future for CC (at least here) seems bleak.”

So is it safe and advisable to invest in these new age internet-based currencies like Bitcoin? Do they pose any real threat to the traditional banking system?

According to a FIAKS expert “, Fiat pegged crypto is the answer to preserving the value of a contract or of your holdings. What that means is that there is a need for financial institutions like banks to back this new age currency if it has to stick for long.” (Fiat money is a currency without intrinsic value that has been established as money, often by government regulation like RBI in India. It was introduced as an alternative to commodity money like a Gold reserve) – (Source: Wikipedia)

He adds, “It’s wrong to assume that currency and regulator are the same. While the regulator (RBI) is concerned with law and consideration paid for a contract is what is measured in currency or equivalent. In case of crypto contract too, if there is a fault, it has recourse to courts just like any other contract.”

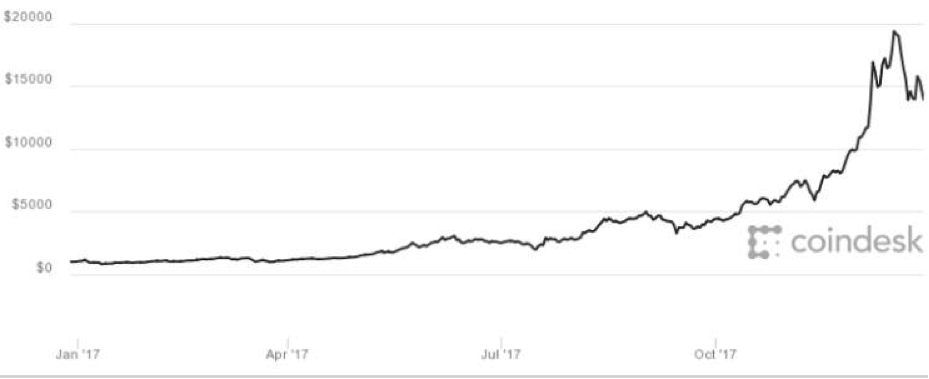

But what about the fluctuation part? To get a perspective, let’s look at the graph below which shows Bitcoin’s historic 2017 price run from $900 to $20,000 (Source Coindesk)

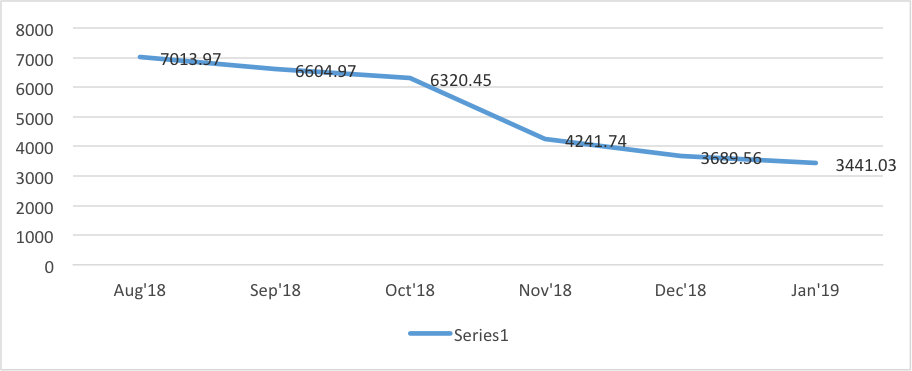

Bitcoin’s growth has a skyrocketing growth at first, but very soon the story changed. In 2018 came what’s known as the Great Crypto crash and Bitcoin’s value fell drastically (more than 70%) in a span of less than a year.

So the question is – Would you invest your hard earned money in a safe thing like a fixed deposit or will you invest it in what some call “the currency of the future” that promises high returns?

Register and read the discussions