Several Founders, Co-Founders, CXO Bankers, CXO Fintech professional & people who participated in the e-panel discussions:

- Mr. Aneesh Khanna, Executive Vice President, NSDL Payment Bank Ltd

- Mr. Kamonasish Aayush Mazumdar, Chief Marketing Officer, MeraEvents

- Mr. Narayan Rao, Chief Services Officer, Suryoday Small Finance Bank

- Mr. Amrish Rau, CEO PayU India, Naspers Group

- Mr. Manish Khera, Founder & CEO, Arthimpact Finserve (P) Ltd, Happy Loans

- Mr. Shirsha Ghosh, Co-Founder, Torit Innovations

- Mr. Ishan Vaish, India Partnership Manager, Apple

- Mr. Shashank Kumar, Co-Founder at Razorpay

- Mr. Fareed Jawad, Principal Architect and Vice President – Payments, FreeCharge

- Mr. Salil Chugh, Global Consulting Practice(APAC) at Experian

- Mr. Riaz Maniyar, Founder & CEO at easy2lend.com

- Mr. Kunal Shah, Founder, and CEO, CRED

- Ms. Arushi Govil, Senior Manager – Legal, PayU Payments Pvt. Ltd.

- Mr. Anupam Varghese, Former Head of Products, EKO India Financial

- Mr. Vishal Anand Kanvaty, Senior Vice President – Products and Innovation, (NPCI)

- Mr. Milind Satpute, VP Product Development, Mosambee – Synergistic Financial Networks

- Mr. John Choudhury, Head – Payments, Partnerships & Co-brand Cards, Flipkart

- Mr. Maunil Gajjar, Manager Projects, Aurionpro

- Mr. Ruchit Jangid, Vice President – eBusiness, Thomas Cook India Ltd

- Mr. Jitendra Gupta, Managing Director, PayU and Founder, Citrus Payment Solutions Pvt. Ltd.

- Mr. Rajiv Rai, Chief Digital Officer, Edelweiss Financial Services

- Mr. Vikas R Panditrao, Co-founder, Forum of Industry Academic Knowledge Sharing (FIAKS)

- Many other CEO/CXO Bankers & Fintech professionals on FIAKS Forum

A lively discussion started in our FIAKS community over the fact that CRED was getting easy access to a part of the 43 million credit card base in partnership with credit bureaus like Experian and CRIF. An expert questioned if they will easily get access to the CC (credit card) base and offer credit against statements. This may lead to the non-existence of the CC business as “Revolve” is one of the major components in CC Profit and Loss. Member explains that CRED is a members-only app which gives out exclusive rewards for paying your credit card bill.

Another question raised by a member was that – Are they getting Credit Card Database? This member thought they only get the Credit Score. They are parsing SMS then. A community member answered that SMS parsing is no longer possible for apps like CRED. CRED gets access to statements on email. Unlike SMS, Email parsing is not possible recurrently.

So what is the principal question here? Since “Revolve” is a major CC Profit and Loss business component, it shouldn’t be disrupted? Only bankers in India can come up with such amazing thought.

An experienced community member believes that CRED is using credit cards to filter the customer. The real model is to leverage payment behavior for lending. Another model is the merchant offers – pushing relevant offers to the right customer base.

A question arose in the midst that if the consumers are giving clear and explicit consent to CRED to access their credit history, then what’s the concern? Another member agrees with this statement. There is no need to be concerned as the consent is given willingly.

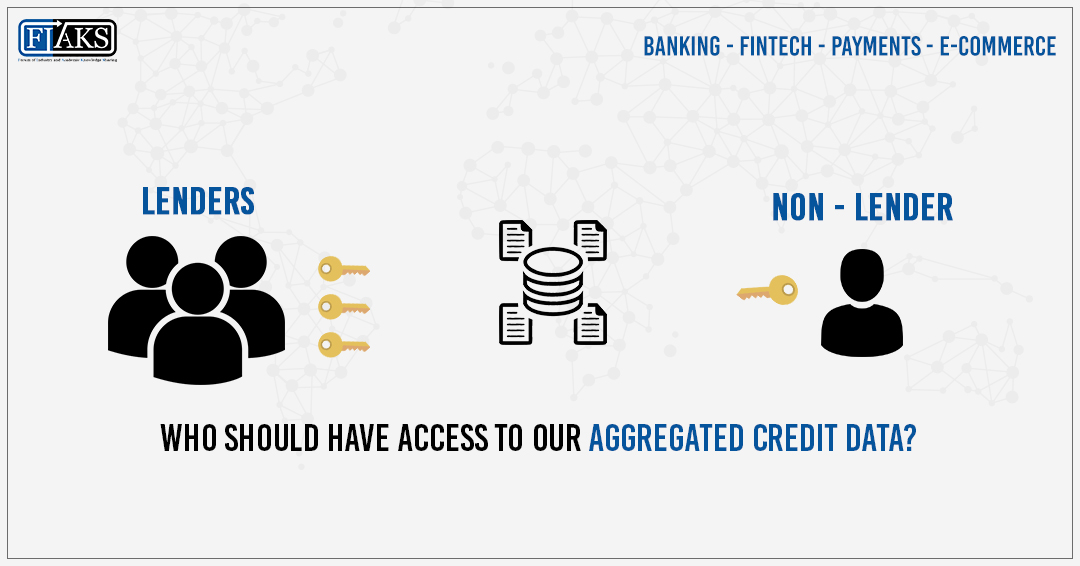

A tenacious issue was brought up by a member about which entities should be allowed to access the credit score. Only entities submitting the information to the credit bureaus (mandated by law) should be allowed or anyone with the customers’ consent?

This question led to a discussion between members. A professional believes that it should be anyone with customer consent. A person’s score with anybody is still that person’s score. The meta is a superset of individual data. Since individual data is being consented, the portion of superset/metaset, where the individual has consented, is accessible to the consented party. But the entities that are submitting, shouldn’t they have privileged access? To which the reply was – they already do. But was promoted as so. People are rising up now. This is not an issue.

Amazon and Flipkart are not making their retail transaction data available. Or Paytm for that matter. Should they be mandated by law to submit the same for anyone to access? And the reply here was that the banks are extremely regressive so it’s not the same. A member reminds us that the credit bureaus have been begging for this data, this first-hand information, for the past 5 years.

Register and read the entire ePanel discussions