Several Founders, Co-Founders, CXO Bankers, CXO Fintech professional & people who participated in the ePanel discussions:

- Mr. Sudhish Sudhakaran, Head of Enterprise Architecture and Applications, Commercial Bank of Dubai

- Ms. Eman Abdellatif, Senior Vice President- General Manager Acquiring Middle East, Network International

- Mr. Probir Roy, Co-founder, Paymate

- Mr. Shashank Kumar, Co-Founder at Razorpay

- Mr. Sharad Goklani, CTO at Equitas Small Finance Bank

- Mr. Rajiv Rai, former Chief Digital Officer, Edelweiss

- Mr. Neeraj Chandra, Head of Operations and Technology, Abu Dhabi Commercial Bank

- Mr. Raghu Veer Dendukuri, Founder, Ideal Nation, and Solution Architect at Invincible Tech Systems Inc.

- Mr. Kamonasish Aayush Mazumdar, Founder & CEO at Foodieverse

- Mr. Ishan Vaish, India Partnership Manager- Worldwide Developer Relations, Apple

- Mr. Deep Shah, Lead- AEPS, NPCI

- Mr. Vikas R Panditrao, Co-Founder, Forum of Industry and Academic Knowledge Sharing (FIAKS)

- Many other CEO/CXO Bankers & Fintech professionals on FIAKS Forum requested to remain anonymous

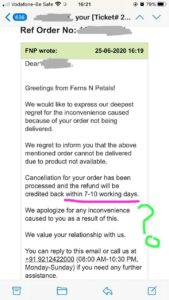

Here’s an image shared by a community member which mentions the refund to be credited back within 7-10 working days:

Thereupon, several questions raised up by FIAKS community are as follows:

Question 1: Why does e-commerce companies require 7 to 10 days to refund money? Is it that all instant payment system is enabled only to collect monies from the customer?

Now here are some mixed viewpoints put forth by the members in this respect:

- One more issue causes the delay, especially for high-value transactions, the refund is considered high-risk transaction especially if not validated with the sale, if the acquiring system does not support the automation validation between sale and refund, the processing team most of the time has to perform the validation manually which cause delay and sometimes they have to call the merchant in high-value transactions to make sure it isn’t fraudulent. Again, effective automation solution.

- Another member states, “the fact is they don’t refund as fast as they debit because they don’t want to. There are two situations. Firstly, failed transactions (the customer gets debited, but the merchant does not see credit) – this results in cancellation after reconciliation as the debit (settlement) does not come through and takes time. Till then the limit is blocked. Here the acquiring bank can initiate a cancellation when they don’t get an acknowledgment of the debit initially, and it would in most cases happen immediately. But they (acquiring bank) don’t build, so it is a faulty process. Secondly, the actual refund should take place immediately as well. But does not because they don’t want to. We keep hearing of the loops that it has to go through. The debit also goes through the same loops and works in a flash.”

- A member made a conjecture, “Well I guess the parties involved in the refund process are the e-commerce company (merchant aggregator), the merchant, merchant’s banker, e-commerce company’s banker, and the customer’s bank. Plus NPCI most likely or an equivalent router. So this 6-way recon may take time. At each level, if it takes T+1 to reconcile and settle back and forth, the refund duration adds up to 7 days, add a couple of days buffer.” In short, it’s all parties as they require reconciliation of the entire transaction before it is refunded, having said that if automation is put in place to reconcile them the timeline significantly reduces to an instant refund for straight-through cases and at a maximum of 2 working days for suspect cases.

- A member opined, “It’s dependent on the operational model of the e-commerce players. Usually, the e-commerce players who are trading on the future availability of the perishable commodities/products face such issues. Because they also don’t own the supply side and totally dependent on the suppliers. Ferns and Petals are one of them. In fact, I’ve faced many challenges regarding the same when I’ve bought vegetables in past from Big basket with 4-5 days gap between delivery and order. Most of these companies’ agreement has included these terms about not deliverables items to which customers have unconsciously agreed to.”

- Another member says, “Generally the e-comm companies do initiate within 3-5 days or within 3-10 days. Once they get the product back. So card to card debit/credit. The time would be split between card issuer/acquirer (maybe even Payment Gateway). Who doesn’t want to hold a float for a day or so maybe more? The question is does it have to be that way. The answer is ‘No’. But if it is a non-credit card payment, I feel it should be near-instantaneous if not a day or two tops. Where the return leg i.e the credit to a customer could be a quick payment channel.”

- A member opined, “Instant refund is possible when refund is handled on a per-transaction basis if NPCI & acquirer bank facilitates to refund the transaction amount along with corresponding transaction fee to the customer, post verification of transaction status on initial payment and post merchant’s confirmation to refund the money.”

Question 2: Why are e-commerce companies displaying products which they cannot deliver?

- Well, to show full catalog might be one reason while a serious problem in the scope of delayed stock update and warehouse sync up is surely possible at times

- Also, poor inventory management, no accurate real-time information on how much inventory which increases the risk of selling non-existent inventory. Market place/the seller should invest in an effective automated solution.

Question 3: How are e-commerce companies enjoying float for 10 days in their account by displaying incorrect information? Who can correct this? Is it the responsibility of the e-commerce company or payment gateway provider or bank sponsoring this program or the regulator?

REGISTER and READ the complete discussions