Non Performing Assets in Banking

Why this Article?

- From 1994 till June 15, RBI has issued nearly 129 circulars on IRAC/NPA. The latest master circular² on the subject is an approx.130 page. This includes number OTS guidelines and guidelines on restructuring of accounts (post-financial crisis, doubling of farm credit initiative of 2004, post-Andhra debt waiver crisis, etc). Recently, they had issued a circular on IRAC after demonetization (Nov 2016). The circular dated 7/2/18 extends some benefits under IRAC for those units affected by GST. Monetary policy statement of 10th February 2018 has indicated that NPA for SMEs will be now 180 days³. Such frequent changes in the guidelines clearly demonstrate that NPA norms cannot be “one size fits all” in the country. It should be recognised that borrowers undergo a lot of financial strain and issues on a day to basis in their business and in their accounts with the banks. Banks should engage with the customer as soon as such strain or stress and default event happen. Banks should not wait for regulatory guidelines to deal with such events or cases. Bank credit is the life line for the borrower and if it is frozen or delayed or drawn back or additional support does not happen then borrower’s business will be affected. A borrower/customer who is subject to financial strain may need additional funds or instant extension of the period of repayment or reduction in the amount to be repaid so that the business continuity is not affected. Delay in rendering such assistance will only aggravate the stress further. The only exception to this the case of wilful defaults.

- I was working in IIBF and used to go for afternoon walks. On more than one occasion, I have seen bankers getting down from a taxi in the gate and rush to a meeting in IDBI (CDR?) for NPA negotiations. Invariably, it will be an issue of “I am in a hurry – I am already late”. Then after some time the corporate owner/officials will come in a chauffeured car. Definitely delayed but not in a hurry. The alacrity with which the security salutes the (defaulting) corporate should be seen to be believed. I wonder why big businessmen are not that much affected by NPA. Is it the corporate veil?

- I have worked in rural branches where borrowers who are BPL will come to the branch to explain why there is a delay in repayment. Those days we did not have NPA but our own DCB (Demand Collection Balance). Their sincerity is worth recalling. Over the next two-three decades, this attitude of theirs will undergo a change when interest and debt waivers, and OTS became the order of the day.

- I was working on a project for strengthening the credit delivery system and was organising a recovery camp. A borrower was very eloquent. He said to the banker; “Sir, there are two loans that I have, one is under IRDP. That’s the government loan. You and I know it need not be repaid. The other one you have given me from your own funds. I will definitely repay that!”.

- Clearly, regulations are necessary for 15% or so defaulters but should all the borrowers go through the pain? As the T&P report says (see box 1 below), the majority of NPA is from corporate accounts. This shows that a very large number of accounts, where repayment is temporarily impaired (SMA 1, 2, etc.) get clubbed with NPA and impacted by norms which are meant for managing the 15% accounts, not the 85% which are not NPA.

The latest report on trends and progress of banks in India says, “Large borrowers who have an exposure of ₹50 million or more accounted for about 86.5 percent of all NPAs, while their share in total advances was 56 percent by end-March 2017. All large borrowal loan accounts with any sign of stress (including special mention account-SMA-0, SMA-1, SMA-2, NPAs, and restructured loans) accounted for about 32 percent of the total funded amount outstanding of PSBs as against 17.4 percent in the case of PVBs. This suggests persisting stress on the asset quality of the banking system”

Possibly this is true of all regulations. Inability to deal with a few recalcitrant borrowers, few money launderers results in the entire country being regulated! So, the impact of IRAC/NPA regulation is that banks cannot or are not allowed to manage NPA. Though the circular says “Board approved policy” there is nothing much for the board to add or subtract and obviously they cannot take a stand contrary to what is in the guidelines. There are two sets of borrowers, i.e. Big and small. Big are capable of taking care of themselves. For them, bank loan, thanks to MCLR regime, is possibly the cheapest source of credit and default induces the banks to take haircut which benefits the big borrowers. Why repay? As against this, as banks have no flexibility, the small borrowers, SME etc. suffer.

There must be substantive reasons for NPA norms. Financial stability is important. Otherwise, the regulator will not pursue them. Possibly the devil is in detail and trying to have one norm for the country and trying to steamroll the process.

Some of the arguments in the following may appear cynical- blame it on my age! Some may be one-sided (how else to get ideas across?) but with justification. It is hoped that arguments that have merits will be considered. Give banks a chance to manage.

How Norms Encourage Defaults?

NPA norms coupled with CDR, restructuring norms and OTS guidelines give ample encouragement for big borrowers/companies to default. The impact of these standard norms on MSME and poor is nothing less than devastating.

Most of the financial sector regulations⁴ are aimed at ensuring financial stability. Viewed in this perspective a one size fits all CRAR, IRAC and exposure norms are, fully justified. It is still too early to conclude if these measures will contain the next crisis. I recall that when Dr. Lahiri was delivering Sir P T Memorial Lecture⁵, we were in Basle I and II then, someone in the audience asked; what after Basle II. Before the speaker could answer I said “Basle III”. Thankfully, he did not mind my intervention. Hardly within a year, Basle III was announced. At that point, we congratulated ourselves that Indian Banking sector has not been impacted by the Global Financial crisis. Was it too early a celebration?

Regulation is “one size fits all ‘if the norms are uniform’ across the country despite the country’s economy, climate, lifestyle, and cash flow volatility differing from region to region. Today, except capital adequacy and priority sector target, all norms apply uniformly to all banks irrespective of the size, business mix and geographical spread of the banks. (When RBI announced differentiated banks, it was hoped that the regulatory norms will also be fully differentiated. Sadly, this is not the case. Barring higher priority sector norms and higher capital adequacy all norms for small finance banks is on par with a full-fledged commercial bank). Regulator seeks full compliance of banks on these issues. Though all RBI circulars ask banks to have Board approved policy the unwritten intention is that the content of the circulars should be approved in the form of policy. Clearly, banks have no discretion to change these norms. It will be nice if these circulars guide bank boards but frame a policy as relevant to their business mix. This, in practice, is not happening. In effect, IRAC guidelines end up micromanaging the banks. Such micromanaging results in unintended distress to many borrowers/clients.

A case in point is NPA norms. NPA norms (see box 2 below) have been adopted for bringing about “international best practices and to ensure greater transparency⁶” in banks financial reporting. (The 133-page master circular on NPA is too much in detail and seeks 100% compliance from banks). One historian while talking about the sculptors of Belur Halabedu Temple wrote that “they started as sculptors but ended as jewellers” for the work was so minute and beautiful. Future historians may not say the same of Basle but say that “They wanted to prescribe regulation but ended writing a detailed manual of operations”. This micromanagement is injurious to banking, commerce, and business of a country.

What are the Non-Performing Assets? (Asset means loans and advances)⁷?

Norms in Brief

A loan or advance is treated as non- performing, in the case of

1. Term Loan Account: wherein interest and/or installment of principal remain overdue (An amount due to a bank under a credit facility is ‘overdue’ if it is not paid on the due date fixed by the bank) for a period of more than 90 days in respect of a term loan.

2. Cash Credit or Overdraft: when the account remains ‘out of order’ due to the outstanding balance remaining continuously in excess of the sanctioned limit/drawing power for 90 days or where the outstanding balance in the principal operating account is less than the sanctioned limit/drawing power, but there are no credits continuously for 90 days as on the date of Balance Sheet or credits are not enough to cover the interest debited during the same period.

3. Bills discounted or purchased: wherein the bill remains overdue for a period of more than 90 days.

4. Agriculture crop loan or term loan: wherein the installment of principal or interest thereon remains overdue for two crop seasons for short duration crops, the installment of principal or interest thereon remains overdue for one crop season for long duration crops,

5. Securitization transaction: wherein the amount of liquidity facility remains outstanding for more than 90 days.

6. Interest receivable: In case of interest payments, banks should classify an account as NPA only if the interest due and charged during any quarter is not serviced fully within 90 days from the end of the quarter.

IRAC norms were introduced two decades back. However, it has been reported that banks have not been very straight forward in this and have been not strict with figures⁸ resulting in reporting the wrong NPA. On account of this NPA, norms have been continuously tightened over the years. In fact, every violation by a bank or two seems to have resulted in the tightening of the norms for the entire banking and finance sector!

The essence of the regulation is that in the case of NPA banks will not recognise income and will also provision for possible non-recovery of unsecured portion of the principal amount. Further, due to the possibility of (a) overstatement of security value or NPA norms or (b) poor collateral efficiency, banks have been advised to maintain a targeted provision coverage ratio. More importantly, even if a bank were to make substantial, but not a full recovery of NPA, the account does not become a standard account. Also, if recovery or collection is made near the time of preparation of NPA statement auditors may ask the bank to continue the account as NPA for some more stipulated time⁹. This rule is meant to avoid possible window dressing by a bank. However, this rule has disastrous implications on a well-intended but defaulting borrower who strives to set right the account because once that is done he/she may be able to operate the account freely. But chances are that he/she/it may be denied further credit due to the above rule.

If the impact of regulatory norms is on the banks alone this article may not be needed. Unfortunately, Banks deviate a bit even in deserving cases resulting in rigid implementation leading into distress of borrowers. Once an account becomes an NPA, albeit for genuine reasons, the banker’s attitude towards that customer changes, that too drastically. NPA can happen due to many genuine reasons. What is genuine and what is not genuine is a matter of interpretation. But the fact of the matter is that even in genuine cases once an NPA has happened it is not possible to help the customer. Some reasons why NPA norms cannot be one size fit all is given below.

Why 90 Days Across Country Is Not Appropriate?

The regulatory circular exhorts the bank to fix realistic repayment. There is a definite hint that banks do not know how to stipulate repayment. It was probably true when commercial banks ventured into financing both working capital and term loan for big companies when they ventured for the first time to finance agriculture. Not anymore! Banks have more than 5 decades of experience in financing all these items. A lot has been learned, a lot has been written off. Interventions like OTP, interest concessions and waivers have wreaked havoc with the credit culture and yet bank lending is taking place and banks are stable.

What is realistic repayment? Is 50% of net take home realistic for a home loan, is 35% of incremental cash flow realistic? Should the DSCR be 1 or 1? Even if there is some agreement on all this, does it mean if the repayment is realistic there will be no cash flow constraints, and loans will be paid exactly as agreed?

It is well known that market interest rates are volatile, commodity prices are volatile, demand & supply of products are volatile and therefore business and firms or individual’s cash flows will be volatile. The degree of volatility and vulnerability to cash flow will be different for the different agro-climatic zone, different industries, etc. It is not possible for banks to anticipate, at the time of sanction, the timing of volatility or its impact on cash flow and factor it while arriving at the repayment schedule for the duration of the loan. Volatility will definitely impact the cash flow and repaying ability resulting in default or NPA unless the borrower arranges other funds to meet repayment commitment. It must be added here that generally; repayment stipulations are made to suit the cash flow. Banks, in general, and PSU banks in particular, seem to adopt uniform appraisal, eligibility and repayment norms across the country¹⁰. It, however, needs no specific proof that wherever there are cash flow vulnerabilities such uniform/standard norms will adversely impact the borrowers resulting in NPA and through them the economy. Thus, it is not banks alone which are impacted by NPA norms and hence the need to voice an opinion.

To aver that NPA, for that matter default may not happen if repayment schedule is realistic is very much unrealistic. Let me not use the word NPA. Let me talk about default or arrears. Default or arrears can happen on account of cash flow volatilities/vulnerabilities due to:

- Business or economic cycles.

- Trade credit tightening in the market and customers defaulting in payment (an ancillary company will default if its parent delays payment and ancillary is never allowed to sell outside!).

- A fire in the business – (settlement of claim takes time and even after settlement -which will be in most cases cover only a portion of losses – there will be losses to be funded) will result in temporary close down of business and will call for fresh investments and recouping of losses. Will these businesses be able to regularise the accounts within 90 days.

- Flood/drought or other issues either which could be statewide or local,

- strike or bandh (which is regular in our country- the recent Koregoan Park, Ghatkopar resulted in huge loss to a few- who will compensate them? What happens if their accounts slip into NPA despite being regular hitherto? The huge losses suffered by business persons and Bus companies, albeit Government companies, due to Padmavat!) Impacting cash flows or destroying business assets,

- Events like AP debt waiver, defaults on account of demonetisation, which impacted small loans – RBI has acknowledged both these events and extended concessions.

- Competition when banks push more finance in the same area for the same purpose. [Two examples: compare the price of a cow after banks started financing dairy units and price of apartments after housing came under priority sector. Bank finance-pushed demand results in a steady and unjustified increase in price. Today two bedroom houses are selling in Mumbai at Rs 2 Crores. How long it will be before defaults start?].

- Rapid changes in technology, which could make the existing business model completely redundant. Remember the half a million-job scheme of early 80’s or financing of PCO Xerox shops (early 90’s) or financing dotcoms (early 2000) all of which suffered due to change of technology. Who needs a PCO when the mobile is handy? If banks had known about mobile banking would they have opened so many branches? How to recoup the loss on such investments? How much time is needed to revive?

- Another reason is inadequate finance. A reading of all guidelines on working capital and the advice to practice MPBF -which is understood as maximum permissible bank finance but in reality resulted in minimum possible bank finance. The objective, when the norms were evolved was to allocate scarce resources- namely credit and lend least amount to the borrower. Despite financial sector reforms, these norms continue. Therefore, in most cases borrower will have to seek private funds which may be at a higher cost. Naturally, debt service will suffer default will occur.

- Two consecutive droughts. It is customary that, in such cases, crop insurance claim is rejected, as the district authorities did not declare drought or the crop cutting experiment did not show crop losses. The doubling of credit initiative announced by GOI in the year 2004 and the follow-up circular issued by RBI and NABARD talk about droughts not declared!

The moot point is that merely fixing realistic repayment does not minimise the possibility of NPA even in GENUINE cases (The word genuine has not been, thankfully, defined), which may face sudden cash flow emergencies/ issues. Borrowers in such cases may default and move to NPA category, as it is simply impossible to arrange for funds merely because they are genuine. In all the above-mentioned cases if the borrower has access to other funds he/she can regularise the account and bank loan can continue, and “they can live happily ever after”. But unfortunately, it is not possible to recoup the losses, insurance settlements are tardy, there are no risk management tools for financial losses on account of business discontinuity due to fire and other hazards and there are no commodity derivatives in agriculture and MSME segments (it has been announced and I hope banks are allowed to use it to protect their portfolio). More importantly, bank credit stops the moment there are any “signals’ in the account. Banks do not finance unless dues are paid, or loans restructured, losses are indemnified/insured and banks deal on a case-to-case basis. CDR is there. But is available to only rich corporates. OTS was offered to small loans. OTS can be extended if the borrower paid a substantial portion of the loan. The small loan borrowers had no access to such funds. As a result, the impact of OTS was minimal.

The above situations may not be true of all accounts at all times. There could be many other valid reasons for cash flow deficiency in business. There could be persons who are affected by one or more reasons. Without a doubt, these cases emphatically point out to the need for differential NPA norms. NPA norm is necessary. NPA policy is necessary. But what it is should be, what its contours should be Board should decide. Given this, if the regulator, at the time of inspection, finds that the framework is inappropriate for the bank then it must penalise the banks. It can give bank-specific directions. It should also ensure that NPA norms do not stop the flow of credit, definitely in genuine cases. It is in the interest of the country that business must flourish.

Evidently, the regulator is aware of all the above reasons and more. A number of concessions given by the regulator from time to time, due to the global financial crisis (2008), subsequent European debt crisis, commodity price crisis, demonetization, GST etc go to support the points made above. Banks have been, through these circulars given permission to restructure debts or extend OTS. CDR is a regulator-approved mechanism for managing defaults in corporate accounts. These circulars are acknowledgments of the fact that business cycle and other reasons will impact the repayment capacity of the borrower.

In the aftermath of Global Financial Crisis banks were allowed to restructure assets. Since the global financial crisis, there have been many occasions when banks had approached the regulator seeking some concession, sectorial relief, rethinking etc. which have not been accepted. Thus, whether the borrowing unit/company is giant iron and steel company or a neighbourhood pan shop, a Rs. 10,000 core limit or a Rs. 10,000 limit, an airline company or an auto-rickshaw, whether a unit is situated in Kashmir or Kanyakumari banks apply the same norm. Banks have not been able to deal with these cases on a case by case basis.

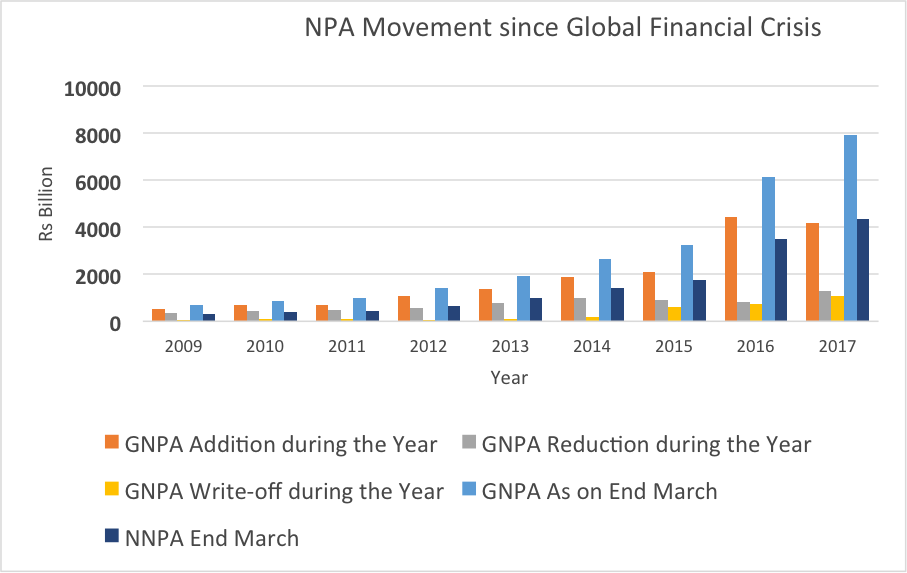

NPA Movement since 200¹¹

Register & Read entire article

Clearly, banks have no discretion in these matters. If the banks are empowered to engage with such borrowers and arrive at viable solutions, there will be no need for the regulator to intervene. Such empowerment will give greater meaning to the banker-customer relationship and also ensure timely relief to honest and well-intended borrowers. More importantly, this will avoid needless concessions in the carb of CDR¹², SDR, and restructuring of assets and the resultant recapitalisation of banks with tax money from public¹³.

Another reason for allowing more leeway for banks to manage their NPA is the way NPA is managed currently.

Generally, banks do not fund their own recoveries. The best way is to recover the dues. Here again, there is a long procedure. No bank can deviate the procedure, such as issuing a routine notice, legal notice, advertisement in the paper etc. which gives ample time to unscrupulous borrowers to divert the assets. In the case of big borrowers, they fly out of the country!

Irrespective of the size and intent of default the bank starts treating the NPA borrower, from the day the account becomes an NPA, differently and almost like an offender. Though regulator has issued a lengthy circular on what is wilful default it is difficult for banks to decide who is willful and who is not. Is the growth of business diversion of funds? What should be the salary of the CEO? What happens if the financial needs of a borrower are more than the exposure limit? Is a flamboyant borrower wilful defaulter? When do you decide ‘wilful default”? Is it before or after exhausting all recovery means? Given that, even if a borrower were to make some repayments in the account and promise to make it regular banks will have to continue to keep them in NPA state for a stipulated time, what is the incentive for the borrower to be regular in repayment? If a borrower avails OTS and pays the loan in full will banks extend one more line of credit? Is it not a fact that OTS and Waivers benefit the recalcitrant borrowers not the regular? Has any FM made a budget announcement to reward the regular farmer or a small loan borrower?

One country one norm. Is it proper?

Let’s take the case of GST. One country one tax. Yet it offers many slabs, many concessions. Some people are exempt, and some are taxed differently. Income tax is another example of which slab is based, offers exemptions, deductions. Only in the case of the financial sector, everything is the same across the country. That’s because of regulations. Regulations happen on account of global compulsions or addressing complaints. If one or two people complain and regulator replies to them or indicates a procedure for that it becomes applicable to all those who are connected with the sector. Case in point is the issue of duplicate demand draft where irrespective of the length of relationship with the bank or amount of deposit held one has to tender an indemnity and two sureties for getting a duplicate. Thankfully it will go out of sight shortly. How many people ask for duplicate draft why not this be left to banks discretion?

Over the years, the banking sector has witnessed many initiatives for NPA management and recovery such as ARC, DRT, Lok Adalat, etc. The crop insurance scheme is in its Nth avatar now. Recently, SIDBI set up CGTSME to partly guarantee the SME loans that are mandated to be issued without any collateral. The guarantee cover varies between 75% to 85% of the default subject to a maximum of Rs 37.50 lakhs in case of loans up to Rs. 50 lakhs. In the case of loans above Rs. 50 lakh and up to Rs. 200 lakhs the maximum guarantee cover will be 50% of the amount in default or Rs. 100 lakh whichever is lower. Member banks will have to bear the remaining amount in default. And there will be a further accumulation of interest from the day a bank applied to the day the amount is approved by CGTMSE because the claim procedure is wrought with many procedural constraints. It is interesting to note that CGTMSE advocates the lending institutions (MLI) to sanction proposals of investment grade and above. Investment grade is medium to high risk. There will be defaults, which get accentuated because of the rule that up to Rs 200 lakhs no collateral should be taken. Banks will not be able to recover the balance, as they have no collateral.

One can infer from the above that the above measures have not been sufficient. Data given by RBI in its report on trends and progress of banking corroborates this view. As of now, the legal procedures favour the defaulter.

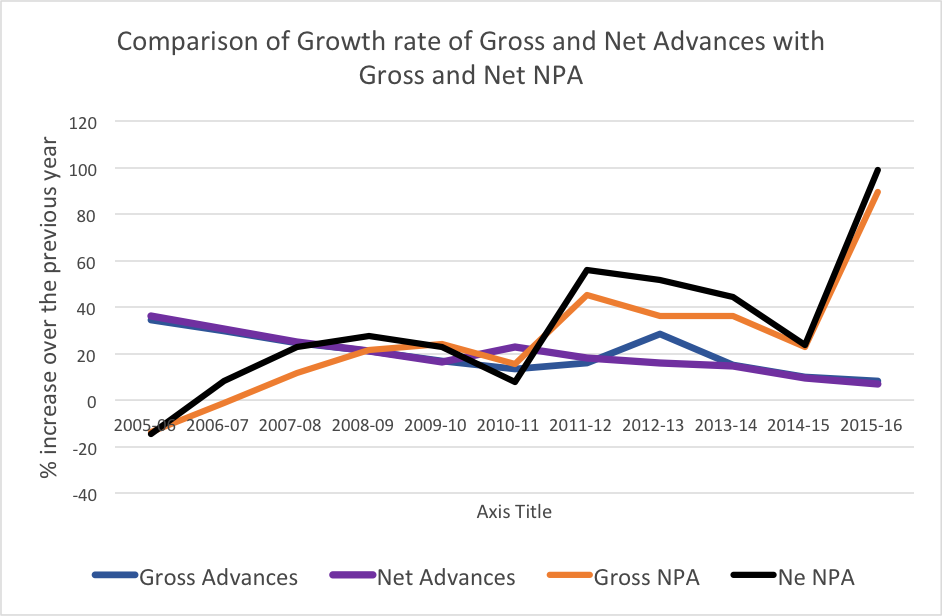

Comparison of the Growth rate of Gross and Net Advances with Gross and Net NP¹⁴

Another method is the sale of NPA to ARCs. Banks can sell NPAs to ARCs. Typically ARC will have to pay some upfront money (10% as per RBI circular) and will get a management fee of 5%. (Previously the fee and upfront money to be paid to the bank were both 5% and it was cash neutral for ARC which could, therefore, buy loans beyond its ability to manage/recover). It has been reported that (a) recoveries have been poor and (b) most of Security Interest is funded by the bank which is selling NPA to the ARC. What should be happening is that having sold the NPA bank will show a better performance in NPA management. Meantime it will show SRs in the investment portfolio. Possibly three years down the line there being no recovery in SRs the bank will have to provide fully for the same.

Another method is the money suit. A money suit takes a long time to decree and the major cause is the endless number of adjournments. I feel that this is due to endless number of adjournments in the cases both by banks advocate as also the advocate of the borrower. No wonder the number of cases is increasing. There is a need to bring a law that there should no more than two adjournments in a money suite filed by banks. No one is better aware of the benefit of adjournment than the borrower who would like to postpone payment as much as possible. DRT was thought of as an innovation. But as the decree can be appealed in the HC it has not been useful. Not allowing appeal is considered against natural Justice!

Another method is CDR. CDR is a mechanism wherein a bank reschedules the dues based on certain terms negotiated with the borrowing company. This method appears slanted in favour of the borrowers/companies. There is a provision in the CDR that whatever the concession was given by a bank the company will kind of give it back once it takes CDR and starts doing well. This has rarely happened! Banks can convert their loans into equity is one option in CDR. One wonders what the status of the bank will be if the company given CDR makes further default. Will they continue to be bankers or treated as part defaulters as owners of equity? This question will arise in the not so distant future.

In practice, CDR is a boon to a company. Once a company comes under CDR it knows that bankers will take a haircut. (Very aptly named for in a haircut you lose your hair and money as well!) The Haircut is recommended in regulatory circulars. Today, many companies may wish they become NPA so that banks will offer them interest and loan concession. Of course, the Government will eventually subscribe to the share capital thanks to taxpayers’ money!

In a sense, it is bigger companies could be beneficiaries of NPA norms and method of managing. The regularity with which default of big borrowers occurs points out a possible strategy¹⁵ of using NPA rules to their advantage. A strategy to reduce the interest burden. Consider a blue chip or a company, which is doing very well. Initially, when they borrow they are able to take a loan at low rates as they are eligible for the best rate that is almost as low as what the depositors get on their hard earned money. Once they default they will get concession in the payment of principal and interest waiver. At best debt will be converted into equity and banks will join them as equity shareholder!

Do the poor have access to CDR? No, they are offered an OTS with interest and principal concession provided they back fully say 75% of the loan outstanding albeit in installments. Most poor do not take it for if they had 75% money they would not have defaulted! If a company is offered OTS or CDR, it can borrow from other sources and comply with the conditions and banks end up with a haircut. In the case of small loans, the borrower cannot meet the 75% or so payment norm as they have no access to other funds. Unless he is a wilful defaulter from where will he bring the funds to meet with the OTS conditions? It appears that OTS for small loans is meant only for wilful defaulters¹⁶. Else poor will have to borrow at an exorbitant rate from moneylenders and repay. How many of the OTS beneficiaries get another dose of a loan? Rarely anyone, if at all.

In this article, I have argued that the current NPA regime favours some big companies. At the same time, given the poor access to funds small loan borrowers are not able to manage the NPA pitfall. There is no doubt that default should be avoided, and banks must manage NPA. At the same time, issues such as the huge restructuring of assets in the recent years, the enormous volume of CDRs, the poor response to OTS of small loans etc. point out to the need to look into the NPA definition and how it is implemented.

One is almost tempted to suggest an alternative to the extant rules. But that will be presumptuous that there could be any unique definition or method which will suit a country as vast as India.

The real issue is that, in the financial stability perspective, can bankers be depended to be true and fair in the assessment of their bad and doubtful debts in the absence of regulation? Shouldn’t NPA norms be on a regional basis? Different for differentiated banks? Different for small loans? Or more simply, shouldn’t banks be allowed to proactively nurse NPA accounts without the auditor/regulator breathing on their back?

One thing that will add immensely to efficient NPA management is collateral efficiency. Cannot the Government restrict the adjournment in bank loan cases to two? Disallow staying of decrees of SARFEASI cases? It is said that insolvency laws will allow quick decisions in the case of NPA? It is doubtful because of how many cases can the bank push to insolvency? (How many of them will knock the High Court doors? Who will decide?) Who will meet the losses on account of insolvency decisions? Should there be a recapitalisation cess?

The objective of this article is not to downplay the NPA problem. It is reported that PSU banks have, over the last 10 years written of Rs. 2.11 lakh crore (Rs 3 Lakh crore between 2009-17) of bad and doubtful debts. During the current year banks, are sitting over nearly Rs. 7 lakh crore stressed assets and NPAs are placed at 17%¹⁷. As such NPA is a big problem facing banks and the country. At the same time, there are issues in the way the NPA norms are being implemented.

Definitely, there is a strong case to review the NPA norms. There is a need to strengthen the appraisal system, improve the collateral efficiency by improving the legal and regulatory environment. Allow banks to take collateral wherever it is available. If it is not done there will be more Debt restructuring and CDR resulting in more haircut for banks for which capitalisation support will come from the Government, eventually taxpayer’s money.

References

¹Written by Dr. R. Bhaskaran. These are his very personal views and does not represent the views or position, on this subject of the organisations that he has worked with or currently associated with.

²RBI 2015-16/101 dated July 1-2015

³As this article goes for publication today, RBI has issued a circular on Resolution Procedures in the process cancelling some circulars on S4A, CDR, etc.

⁴There are more than 40 master circulars issued to banks by RBI on various subjects. Each of them contain many pages of instructions

⁵INDIAN FINANCIAL REFORMS: NATIONAL PRIORITIES AMIDST AN INTERNATIONAL CRISIS Sir Purushotamdas Thakurdas Memorial Lecture organized by IIBF Dr. Ashok K. Lahiri, Executive Director, Asian Development Bank, Manila on January 16, 2009, at Mumbai.

⁶Wikipedia

⁷For details please refer RBI circular

⁸Whenever a PSB has witnessed a change of guard at the top, their immediate quarterly performance has nosedived. http://www.rediff.com/business/report/pix-special-reasons-behind-the-failure-of-indias-public-sector-banks/20150312.htm

⁹RBI in its circular says “Accounts regularised near about the balance sheet date: The asset classification of borrowal accounts where a solitary or a few credits are recorded before the balance sheet date should be handled with care and without scope for subjectivity. Where the account indicates inherent weakness on the basis of the data available, the account should be deemed as a NPA. In other genuine cases, the banks must furnish satisfactory evidence to the Statutory Auditors/Inspecting Officers about the manner of regularisation of the account to eliminate doubts on their performing status.

¹⁰ Possibly the fear of vigilance has made PSU’s adopt uniform credit norms across the country.

¹¹Statistical Tables relating to Banks in India. Table 7 Movement of NPAs of SCBs: RBI https://dbie.rbi.org.in/DBIE/dbie.rbi?site=publications#!4

¹²“This scheme is in no way a cure-all for Indian banks’ deteriorating asset health — instead it exacerbates the risk by deferring an estimated (Rs 1.5 lakh crore) of NPA formation from (2015-16/2016-17) to later years,” Religare said, adding it expects many SDR cases to fail, resulting in high and chunky slippages in 2016-17 and 2017-18.-http://indianexpress.com/article/business/banking-and-finance/strategic-debt-restructuring-scheme-a-solution-with-its-own-problems

¹³Given that majority of the stressed assets are on the books of public sector banks, more pain will be visible on their balance sheets going ahead. This would also mean higher capital requirement for these lenders since current norms require banks to set aside huge amounts of capital to cover stressed assets. http://ggiforum.com/index.php/law/debt-collection-insolvency/606-corporate-debt-restructuring-a-new-fad-or-path-to-future-destruction

¹⁴Data Source: RBI

¹⁵Of late, it is found that unscrupulous borrower companies are diverting, misusing siphoning their funds for the personal benefit of directors/promoters. This is being done with a view to taking undue advantage of CDR Mechanism which has been causing heavy losses not only to public sector Banks , FIs, Private sector Banks but also other creditors and stakeholders: http://taxguru.in/corporate-law/corporate-debt-restructuring-mechanism-review-redefine-policy.html

¹⁶Managing defaults in small loans and agricultural accounts. R. Bhaskaran. IIBF – archive of monthly column.

¹⁷Even as the government has been trying to shore up public sector banks through equity capital and other measures, bad loans written off by them between 2004 and 2015 amount to more than Rs 2.11 lakh crore. More than half such loans (Rs 1,14,182 crore) have been waived off between 2013 and 2015. – See more at: http://indianexpress.com/article/india/india-news-india/bad-loan-financial-year-rti-rbi-bank-loan-raghuram-rajan-bad-loan-financial-year-rti-rbi-bank-loan-raghuram-rajan-1140000000000-bad-debts-the-great-govt-bank-write-off/#sthash.X9DPH2kK.dpuf

About the Author

Dr. R. Bhaskaran has more than 4 decades of experience in the field of banking and finance, and training and development. He started his career as an officer with Bank of India. From there he moved on to NABARD where he has worked in project appraisal, credit delivery system, fund and treasury management, Joint Director and Director in charge of Bankers Institute of Rural Development (BIRD) and CGM looking after cooperative banking and later institutional development. He left NABARD and took over as CEO of Indian Institute of Banking & Finance where he worked for 10 years. He was member of RBI committee on

Institute of Banking & Finance where he worked for 10 years. He was a member on the RBI committee on capacity building of banks and NBFC. He is currently an independent board member and Chairman Audit Committee of a bank in Bhutan. He is a Member of Technical Committee Financial Accreditation Agency of Malaysia and Member of Board of Supervision of NABARD.

Disclaimer: This section is a compilation of news, articles, updates and information (“Updates”) related to payments,fintech, banking and other industry. All Updates belong to the source provided after every such Update. FIAKS does not have and in no manner claims to have any intellectual property rights in the content, images, pdf, videos etc. in any of the Updates. This section has been created for knowledge sharing/education purposes for our smart FIAKS communities across the globe. We understand that the fair use of a copyrighted work or work protected under any intellectual property law, including such use by reproduction in copies or by any other means specified under applicable laws, for purposes such as criticism, comment, news reporting, teaching (including multiple copies for classroom use), scholarship, or research, is not an infringement of copyright. This section and our website may contain certain copyrighted or the work otherwise protected under any law that were not specifically authorised to be used by the copyright holder(s) or right holder(s) but which we believe in good faith are protected by the applicable laws and the fair use doctrine for one or more reasons noted above. If you have any specific concerns about this section or our website or our position on the fair use defence, please contact us at contactus@fiaks.com so we can discuss amicably. Thank you.